Almost anyone can initiate budgeting; however, saving money initially seems rather tricky. Saving is spending money on needs, wants, and savings goals. Here are some simple tips to enable investors to save according to the current economic status.

1. Use the 50/30/20 Rule

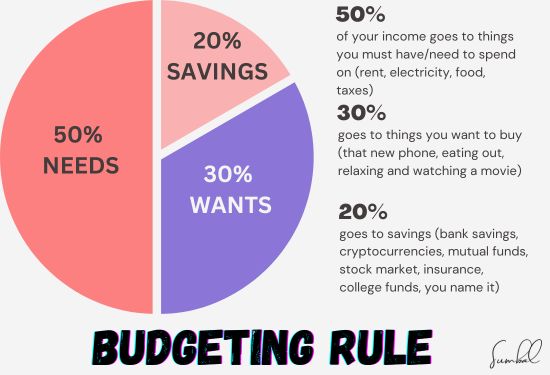

This approach recommends allocating your income in the following way:

50% to Needs

These are the core expenses you need, like housing, food, power, gas, and the maintenance of vehicles.

30% to Wants

This portion is used on desires but necessary items such as eating out entertainment, and hobbies.

20% to Savings or Debt Repayment

This is the most crucial step because it helps accumulate the amounts needed to provide a favorable financial situation and avoid stress.

Applying the 50/30/20 rule makes budgeting easier by allowing you to track spending. If reducing your spending by 20% is possible, begin with a small amount. Setting aside as little as 5-10% for savings will still count in the long run and prepare you to develop good financial practices.

2. Set Clear Goals

Saving money works best when it's linked to clear objectives. Establishing clear short, mid, and long-term goals is the first stage. Short-term goals include saving for a trip or creating an emergency fund. The short-term objective could be having a certain amount of money for a down payment on a car, while the long-term aim could be saving for retirement or a home.

After envisioning your goals, segment them into smaller achievable goals along the monthly or weekly plan. For instance, if you aim to save $1000 in 6 months, you should save about $167 monthly.

3. Automate Your Savings

Saving is one of the most manageable tasks to perform in the comfort of an automated environment. Move from your checking account to a savings account automatically. It is easier to avoid spending money on unnecessary items, especially when saving is a vital expense.

Some popular banking options allow transactions to be rounded to the nearest dollar, with the change going to a savings account. This way, each time you set aside some money, it accumulates automatically without one realizing the progress made towards creating sufficient savings.

4. Cut Unnecessary Expenses

You should observe the structure of your expenses for a month and see what you can eliminate. It might be worth leaving them and dealing with them less frequently. Reducing the frequency of eating out or limiting one’s tendencies to buy unnecessary things can also create extra cash that will go into savings.

We should make coffee at home, cook meals, make a shopping list, and buy groceries rather than stopping by Starbucks, McDonald's, or the supermarket and buying food on impulse. As you know, a slight change in everyday spending can lead to saving much more in a few months or years.

5. Track Progress and Celebrate Wins

Progress is tracked to stay motivated. You should have a simple chart to track your savings progress. This may be an Excel spreadsheet, a designed application, or even an old paper notebook. It keeps the savings culture active and motivates many people.

There is no harm in celebrating small accomplishments, like hitting your first $500 or your first $1,000. Afterward, you should treat yourself to a small meal because motivation is crucial when following a plan.